MAP Views Second Quarter 2025

Apr 01, 2025The first quarter of 2025 proved to be a volatile one for the financial markets and global currencies. Stock prices seemingly gyrated with every tweet and announcement from POTUS. Talk of tariffs sent U.S. stock prices lower, and the dollar higher. Whereas talk of delayed tariffs had the opposite effect. The volatility coming out of Washington has created a swath of geopolitical and economic uncertainty, an environment the markets do not appreciate.

Perhaps the most interesting trend during the quarter was how quickly stock market darlings from 2023 and 2024 turned into laggards. The fourth quarter of last year marked a peak in American Exceptionalism. Following November’s elections, U.S. stocks soared along with the dollar as investors bet lower taxes and less regulation would propel domestic growth. Lofty expectations for Artificial Intelligence (AI) propelled prices of the Magnificent Seven (Mag 7) stocks even higher. On the back of the Mag 7 stocks, the S&P 500 posted its best 24-month run in history for the period ending December 31, 2024. As 2024 wrapped up, the S&P 500 carried a valuation of 24.0 times trailing earnings. Historically, when inflation was in the three percent range (an environment we are currently in), the price/earnings multiple was closer to 17.0 times.

The past three months have also brought a touch of reality back to U.S. valuations, highlighting the attractiveness of international valuations. In fact, this quarter marks the worst relative performance for U.S. stocks relative to global markets in 23 years. On a total return basis, while the S&P 500 was down 4.27% for the first quarter ending a streak of five straight winning quarters, the MSCI ACWI declined just 1.22%. Within the S&P 500, there was a wide variance in the performance among the many sectors. As an example, Information Technology fell 12.65%, led by the Mag 7 down 14.72%, while Consumer Staples and Healthcare were up 5.23% and 6.54%, respectively. The Nasdaq Composite declined 10.26% during the quarter on a total return basis, its worst quarter since Q2 2022. This is contrary to the last two years when technology ruled the day, and more defensive sectors languished, despite a margin of safety. Furthermore, the S&P 493, up 1.02% (total return) for the quarter, outperformed the S&P 500 by 529 basis points, additional evidence of the reality we mentioned.

Source: Bloomberg

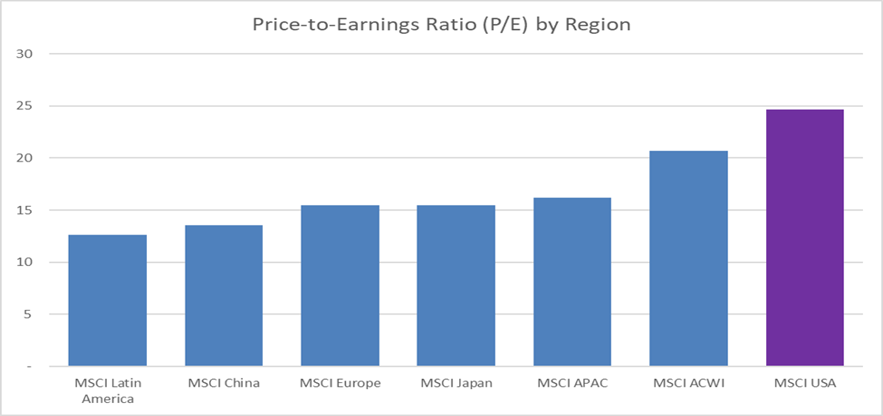

For comparison purposes, as the chart on the previous page illustrates, indices outside of the U.S. are much more attractive on a relative basis. Late last year, an attendee at a presentation we delivered stated: “Europe is uninvestable!” Their justification was that the U.S. innovates, and Europe regulates. Our rebuttal was that everything has a price. The U.S. market was priced to perfection (as we all know, utopia does not exist in the financial markets), and Europe was pricing in a dire future.

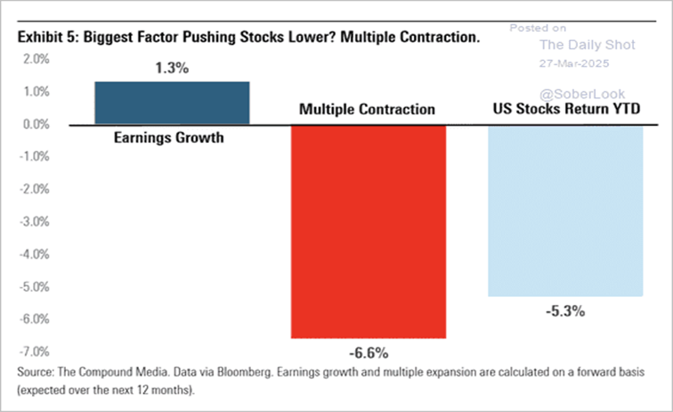

As we mentioned in several recent webinars and thought pieces, valuation expansion significantly contributed to the strong returns of the U.S. equity markets in 2024, leaving little if any margin of safety. Fast forward to today, and the largest contributor to the declines in the broader markets has been valuation contraction, as seen in the chart below.

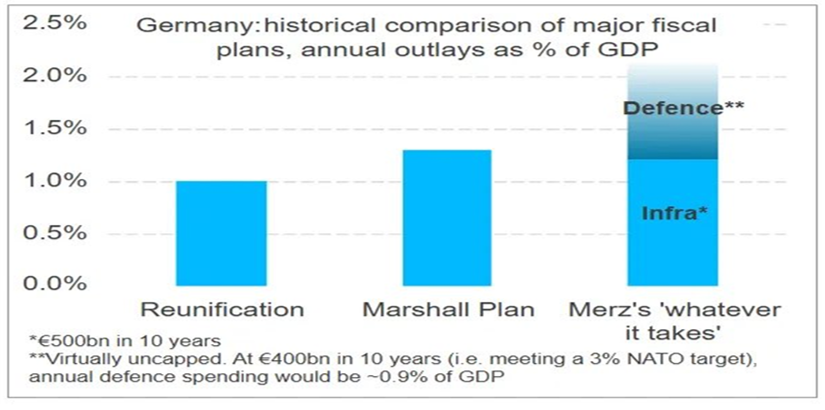

Outside U.S. borders, investors have been asking what the investment landscape will look like should the war end in Ukraine. We believe European energy prices would likely fall, easing inflationary pressures. However, Ukraine will require a multi-year/multi-billion-dollar rebuild effort. Unlike the previous administration, the U.S. has stated its discontent with funding that bill. In doing so, POTUS has ultimately forced Europe to fund these efforts. As we have witnessed in the U.S. over the past several decades, spending money is stimulative to the economy. We believe Europe may be in the initial stages of a substantial economic rebound as spending increases. For years, the U.S. ran billion dollar plus deficits, while Germany had a balanced budget. As shown on the following page, a recent spending plan passed by the Bundestag (the lower house of Germany’s parliament) is larger than the German Reunification plan of the early ‘90s and the Marshall Plan (adjusted for inflation). The Marshall Plan was instrumental in rebuilding Europe post World War II. Given the fact that European shares have been under-owned and unloved for so long, we believe European equities will see a revival and the runway may be a long one. For more information on this subject, please read our most recent thought piece.

Source : https://www.icis.com/. *Infra stands for Infrastructure.

We believe an environment of heightened geopolitical and economic uncertainty strengthens the case for active management. In the recent past, investors have been rewarded for taking the “easy path.” Simply buying passively managed, exchange traded funds that invested in the stocks of the S&P 500 or the NASDAQ 100 generated stout returns, as a rising tide floated all ships. The outsized weightings of the Mag 7 helped drive these generous returns. We strongly believe that what worked for the past few years will not work for the next few years. While we monitor, we do not act on the seemingly daily barrage of tweets and announcements coming out of Washington. Rather, we look at the bigger picture. The Investment Team believes the picture is that the U.S. dollar will trend lower over the next few years. And while this trend will likely not occur in a straight line, we believe it should benefit select foreign stocks, multinationals, and material/commodity shares.

As we proudly celebrate MAP’s 25th anniversary later this year, we truly appreciate the confidence our clients place in us. Our team has remained disciplined and resists the allure of fleeting fads as we are steadfast with a well-defined investment strategy, as evidenced by the risk-adjusted returns we have generated over complete market cycles. Given today’s economic and geopolitical landscape, we believe these attributes are more important than ever.

Think Spring!

Managed Asset Portfolios Investment Team

Michael Dzialo, Karen Culver, Peter Swan, Zachary Fellows, John Dalton, and Nicolas Vilotti

April 2025

Certain statements made by us may be forward-looking statements and projections which describe our strategies, goals, outlook, expectations, or projections. These statements are only predictions and involve known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those expressed or implied by such forward-looking statements. The information contained herein represents our views as of the aforementioned date and does not represent are commendation by us to buy or sell this security or any other financial instrument associated with it. Managed Asset Portfolios, our clients and our employees may buy, sell or hold any or all of the securities mentioned. We are not obligated to provide an update if any of the figures or views presented change.