Navigating The Tariff Tantrum

Apr 08, 2025With stock prices plunging, it is logical to wonder: “why not move to cash until the tariff tantrum ends?”

We equate the current scenario to the early weeks of the COVID-19 crisis. Stocks tumbled as the virus spread and the economy ground to a halt. Many clients called wanting to move to cash, indicating that “the stock market will never recover until there’s a cure for COVID.” There still is not a “cure,” but even before there were treatments, the stock market began to take off.

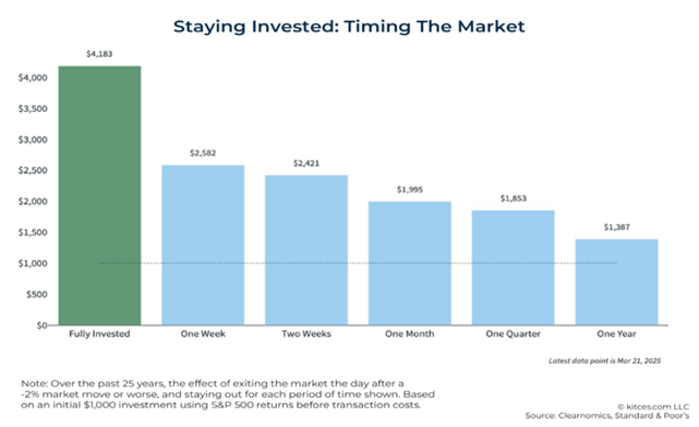

The stock market is a leading indicator. The worst financial decisions are made under panic scenarios. As the chart below depicts, those who exit the market the day after every –2% market move or worse over a 25-year time period consistently underperform those who remain fully invested, regardless of how quickly they return to the market. If anyone can pick the best days to be invested, they are extremely lucky and should probably make their way to Vegas. The fact is that "time in the market, not timing the market" is the more reliable path to long-term investment success.

Further compounding the dilemma of moving to cash is that rallies usually begin in the darkest of times. During COVID, stocks found a bottom when the virus was still ravaging the world and all, but non-essential businesses were closed. The same can be said for the Great Financial Crisis (GFC). Stocks began their ascent, before the economy began to recover.

What actions/events could make the markets rebound from the tariff tantrum?

- Market weakness could force the Federal Reserve (the Fed) to lower interest rates. While this might be a bitter pill for the Fed to swallow, we would not bet against it, especially if the financial system becomes crippled due to declining asset prices (think Long-Term Capital Management (LTCM) back in 1998).

- Some countries strike deals with the Administration to lower tariffs. Current reports state that over 50 countries have reached out to begin negotiations.

- Tariffs might get derailed or delayed by the courts. Additionally, some companies might get a break for agreeing to multi-billion-dollar investments in the U.S.

- And lastly, the economic disruption caused by the tumbling stock market increases the odds that 2017 tax cuts get extended and new tax cuts get passed (i.e., no taxes on Social Security, tips, or overtime). This could help to stimulate the economy and lessen the negative impacts stemming from tariffs and lower stock prices.

Obviously, certain companies and industries will be more impacted by tariffs than others. The price action on April 3, 2025, in our opinion, did a fairly decent job of sorting out which companies will be hurt the most and those that should suffer less. The declines on April 4, 2025 appear to be more along the lines of “throwing the baby out with the bathwater.”

We believe this may be a result of some investors (particularly hedge funds) being highly leveraged and forced to sell what they can, not necessarily what they want to, in order to cover margin debt.

Bottom line, stock market retreats are never enjoyable, but they do happen. It is imperative to think logically and rationally. It is impossible to predict the next tweet or post, but we can position portfolios to take advantage of opportunities we see, as well as sidestepping some of the risks that are present as well, as we strive to deliver superior risk-adjusted returns. Overall, we believe U.S. valuations can continue to move lower along with the U.S. dollar, especially with equity risk premiums favoring foreign markets relative to U.S. markets.

We encourage you to contact your MAP representative with any questions or concerns.

Managed Asset Portfolios Investment Team

Michael Dzialo, Karen Culver, Peter Swan, Zachary Fellows, John Dalton, and Nicolas Vilotti

April 8, 2025

Certain statements may be forward-looking statements and projections which describe our strategies, goals, outlook, expectations, or projections. These statements are only predictions and involve known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those expressed or implied by such forward-looking statements. The information contained herein represents our views as of the aforementioned date and does not represent a recommendation by us to buy or sell this security or any other financial instrument associated with it. Managed Asset Portfolios, our clients and our employees may buy, sell, or hold any or all of the securities mentioned. We are not obligated to provide an update if any of the figures or views presented change. Past performance is no guarantee of future results.